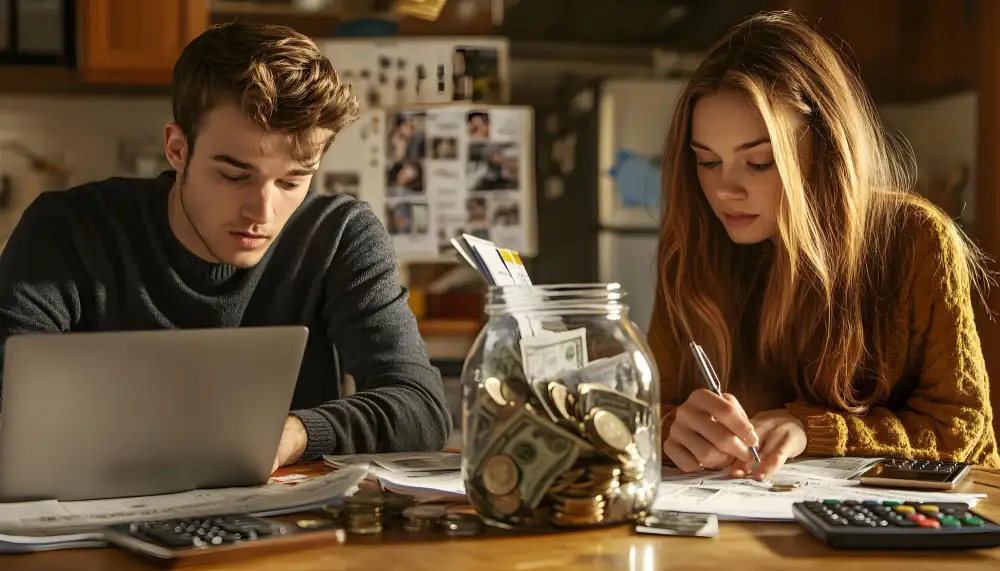

Managing finances is often the most daunting task for students transitioning to independent life. The foundation of financial freedom is not necessarily how much you earn through part-time work or stipends, but how effectively you manage what you already have. A well-structured budget is a roadmap that prevents the inevitable mid-month panic when the bank account balance starts looking dangerously thin. In 2025, with rising inflation and the increasing cost of living, understanding where every single penny goes is more critical than it has ever been for the average university student.

A popular and highly effective method for beginners is the 50/30/20 rule. However, in a student context, this often needs to be adjusted to a 60/20/20 or even a 70/20/10 split depending on local rent prices. Ideally, 50% of your total income—whether it comes from parents, government loans, or a job—should go toward absolute needs. This includes rent, basic groceries, utilities, and essential transport. The next 30% is allocated for "wants"—socializing, dining out, streaming subscriptions, or hobbies. The remaining 20% should be tucked away into a high-yield savings account or used to aggressively pay off high-interest debt like credit cards.

You cannot manage what you do not measure. In the digital age, there is no excuse for not tracking expenses. Whether you prefer sophisticated apps that sync with your bank or a simple manual spreadsheet, logging every coffee, bus ticket, and late-night snack is essential. Many students are genuinely shocked to find they spend hundreds of dollars a year on "ghost subscriptions"—services they signed up for once and never used again. By reviewing your spending at the end of each week, you can identify patterns and find areas where you can cut back, such as switching from premium brands to store-brand alternatives at the supermarket, which can save up to 40% on your weekly grocery bill.

Long-term financial habits are built in your twenties. Budgeting is a marathon, not a sprint. Setting small, achievable goals, such as saving just $50 a month, builds the psychological discipline required for later life when the financial stakes are much higher. Remember that a budget is not meant to be a cage that restricts your fun; rather, it is a tool that ensures you can enjoy your social life without the crushing stress of being unable to pay your rent or buy textbooks at the end of the semester. Start early, stay consistent, and treat your budget as a living document that evolves with your needs.

Furthermore, consider the "envelope system" for discretionary spending. If you struggle with overspending on nights out, withdraw a specific amount of cash at the start of the week. Once that cash is gone, your "fun budget" is exhausted until the next week. This physical limitation helps ground your digital spending habits. Additionally, always look for student-specific banking accounts that offer no-fee structures and better interest rates. Many banks compete for student loyalty, offering sign-up bonuses or better terms for those currently enrolled in higher education. Leveraging these perks is a smart move that adds up over the course of a four-year degree.